Monthly bookkeeping can mean very different things depending on who does it. Some providers simply code transactions as they come in. Others run a full month-close process that produces reliable reports you can actually use. For small business owners in Los Angeles and across California, the difference matters—because the goal isn’t “numbers in the software.” The goal is clean, reconciled books that support decisions and make tax season predictable.

Below is a clear, client-facing breakdown of what monthly bookkeeping means in plain language, what deliverables you should expect each month, what “done right” looks like, and what is typically outside the scope unless you add it on.

If you’re comparing providers, start with what the outcome should be: consistent month-close and dependable reports. That’s how we structure our bookkeeping services.

What “Monthly Bookkeeping” Means (Plain Language)

Monthly bookkeeping is a recurring process that takes your real-world activity—bank and credit card transactions, deposits, transfers, payments, refunds, and other financial events—and turns it into a clean set of records for a specific month.

It is not only “data entry.” Done properly, it answers three practical questions:

- Did we capture everything? (Nothing missing, nothing duplicated.)

- Is it categorized correctly? (The transaction belongs in the right account and category, consistently month to month.)

- Do the totals match reality? (Balances tie to bank and credit card statements after reconciliation.)

When those three items are true, your reports are reliable. When they are not, the reports may look “reasonable,” but they can be materially wrong—and that’s when owners get surprises later.

Monthly Deliverables: What You Receive

Most owners want two things: clarity and confidence. The deliverables below are the core outputs of a properly managed monthly cycle.

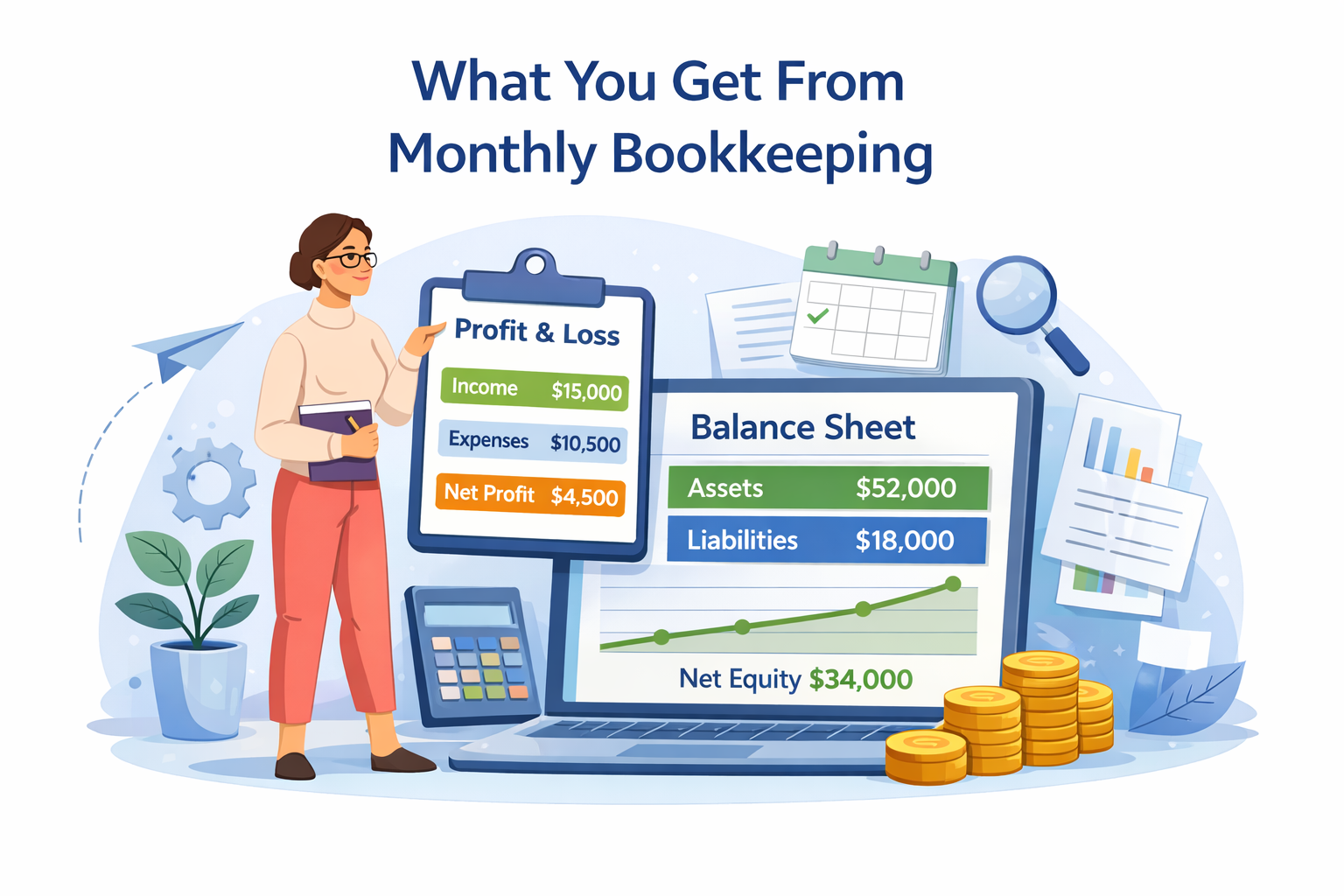

1) Profit and Loss (P&L)

What it is: A summary of revenue and expenses over a period (typically month-to-date and year-to-date).

What owners use it for:

- Understanding profitability (not just sales volume)

- Monitoring major expense lines and cost trends

- Comparing months and evaluating performance

- Making decisions on pricing, hiring, and overhead

What “done right” looks like:

- Revenue and expenses are recorded in the correct month (not shifted by timing errors)

- Categories are consistent, so trends are real (not “noise” from changing labels)

- One-time items are handled cleanly, so operating performance is not distorted

A P&L becomes genuinely useful when it is stable. If categories change each month—or if key expenses are misclassified—your “trend” analysis becomes misleading.

2) Balance Sheet

What it is: A snapshot of what your business owns and owes at a point in time: cash accounts, credit cards, loans, payables, and equity.

What owners use it for:

- Confirming bank and credit card balances are correct after reconciliation

- Tracking liabilities (cards, loans, and other obligations)

- Supporting financing conversations (lenders often request Balance Sheets)

- Ensuring the books are structurally sound (not hiding issues in “misc” accounts)

What “done right” looks like:

- Balances tie to statements for bank and credit card accounts

- Loans are tracked properly (principal vs. interest, correct liability balances)

- Owner contributions/distributions are recorded consistently

- Uncategorized/suspense balances are kept minimal and resolved, not ignored

Many bookkeeping issues show up first on the Balance Sheet. If the Balance Sheet is messy, the rest of the financial picture is usually questionable.

3) Cash Flow View (Cash Flow report and/or Cash Summary)

What it is: A view of how cash moved—what cash came in, what went out, and what changed the bank balance. Depending on the business and reporting setup, this can be a formal Cash Flow statement or a management-style cash summary.

What owners use it for:

- Understanding why profit does not equal cash in the bank

- Spotting cash pressure early (before it becomes a problem)

- Planning upcoming payments, taxes, inventory, and payroll

What “done right” looks like:

- Transfers are not double-counted as income/expense

- Credit card payments are recorded in a way that does not distort expenses

- Owner draws and contributions are clearly separated from business operations

Fix this in your books

If you’re not sure where to start, we can help. We’ll review your current bookkeeping setup, identify any gaps or issues, and give you a clear plan to fix it — just straightforward advice.

Quality Checks: What “Done Right” Means

“Clean books” is not a slogan. It’s the result of specific checks that reduce risk and make the numbers dependable. Here are common examples of what gets reviewed during a professional monthly cycle.

Reconciliation (Non-Negotiable)

Reconciliation is the process of matching your bookkeeping records to external statements (bank and credit card). This is the verification step that confirms completeness and accuracy.

Examples of what reconciliation catches:

- Missing transactions (fees, interest, refunds not recorded)

- Duplicates (imported twice, or imported + manually entered)

- Timing problems (items posted in the wrong month)

- Incorrectly recorded transfers (treated as revenue/expense)

If accounts aren’t reconciled, reports can look fine while still being wrong. Reconciliation is what turns “likely” into “verified.”

Duplicate and Missing Transaction Checks

Examples:

- A Stripe/merchant deposit appears twice in the feed

- An expense is missing because a new card wasn’t connected

- Refunds and chargebacks were recorded in a way that inflates revenue

These issues are common and they directly affect profitability, tax estimates, and decision-making.

Mis-categorization and Consistency Review

We check for category drift and classification errors that make reports less useful:

- Meals vs. marketing vs. subcontractors being mixed month to month

- Software subscriptions scattered across multiple unrelated categories

- Personal transactions mixed into business activity (or business expenses excluded)

- Large items assigned to generic buckets that hide what they really are

Consistency is what makes your reports comparable over time. The goal is not perfection—it’s reliability.

Uncategorized / “Ask My Accountant” / Suspense Review

Any file can look clean if everything questionable is dumped into a catch-all account. A quality month-close reduces these items and resolves them using documentation, client clarification, and clear rules for future months.

Reasonableness Check (Reality Test)

Finally, there’s a practical review that asks: does this make sense for your business?

- Does revenue align with your sales activity?

- Do payroll or contractor costs match headcount and pay schedules?

- Are margins plausible for the industry?

- Do liability balances (loans/cards) move as expected?

Timeline: When the Numbers Become Final (Month Close)

Professional monthly bookkeeping includes a clear month-end close: a point when the records for that month are considered finalized.

A typical cadence looks like this:

- Days 1–10 of the new month: finalize late-posting transactions, collect missing receipts, resolve unclear items

- Days 10–20: reconcile accounts, complete quality checks, prepare reports

- After close: numbers are treated as final unless new information appears (late bank posting, corrected invoices, etc.)

The important part is predictability: you should know when you’ll receive finalized numbers, and what’s needed from you to close the month without delays.

If you want to compare service levels and what’s included, see our monthly plans.

What’s Typically NOT Included (Boundaries)

Monthly bookkeeping is the foundation, but it does not automatically include every finance-related task. Clear boundaries protect both the client and the process.

Common items not included unless explicitly added:

- Tax filing and tax strategy

- Payroll processing and payroll tax filings

- Sales tax filing (CDTFA)

- Invoicing/collections (accounts receivable management)

- Bill pay (accounts payable management)

- CFO-level forecasting and investor reporting

- Historical corrections beyond the agreed cleanup window

- Entity formation filings and legal services

- Detailed inventory cost tracking (depends on the business)

What Changes for the Owner

When monthly bookkeeping is done consistently and correctly, the impact is practical:

Better decisions, faster

- Know whether you’re actually profitable (not just busy)

- See where costs are increasing before it becomes a problem

- Make hiring and marketing decisions based on dependable numbers

Fewer surprises

- Less last-minute cleanup at year-end

- Fewer “why is the tax bill so high?” moments

- Less stress during audits, financing requests, or partner reviews

Tax-ready and handoff-ready books

- Reconciled accounts

- Consistent categorization

- Clear owner activity

- Organized support for exceptions

A Simple Monthly Checklist

- Bank and credit card accounts reconciled

- Transactions categorized using consistent rules

- Uncategorized/suspense items reduced and resolved

- Month close completed (with a clear close date)

- Reports delivered: P&L, Balance Sheet, Cash Flow view

- Notes provided: exceptions, missing items, and client action points

«Three Common Bookkeeping Mistakes Small Business Owners Make».

«Why Every Business Needs Bookkeeping».

<div id="visit-counter" style="margin-top: 16px;"></div>

Related services

See how ongoing bookkeeping works.

Fix old months before they create bigger problems.

Compare bookkeeping, QuickBooks, payroll, and reporting support.