Many business owners think their books are “clean” if transactions are categorized and the Profit & Loss shows some numbers. But real clean books mean much more: your financial picture is accurate, complete, tax-ready, and free of hidden surprises that can appear during an audit, loan application, or tax filing.

“Clean books” in plain owner language: you (and your accountant) can trust every number. There are no duplicates quietly inflating expenses, no missing deposits making revenue look lower, no personal expenses disguised as business ones, and reports match reality when someone looks closely.

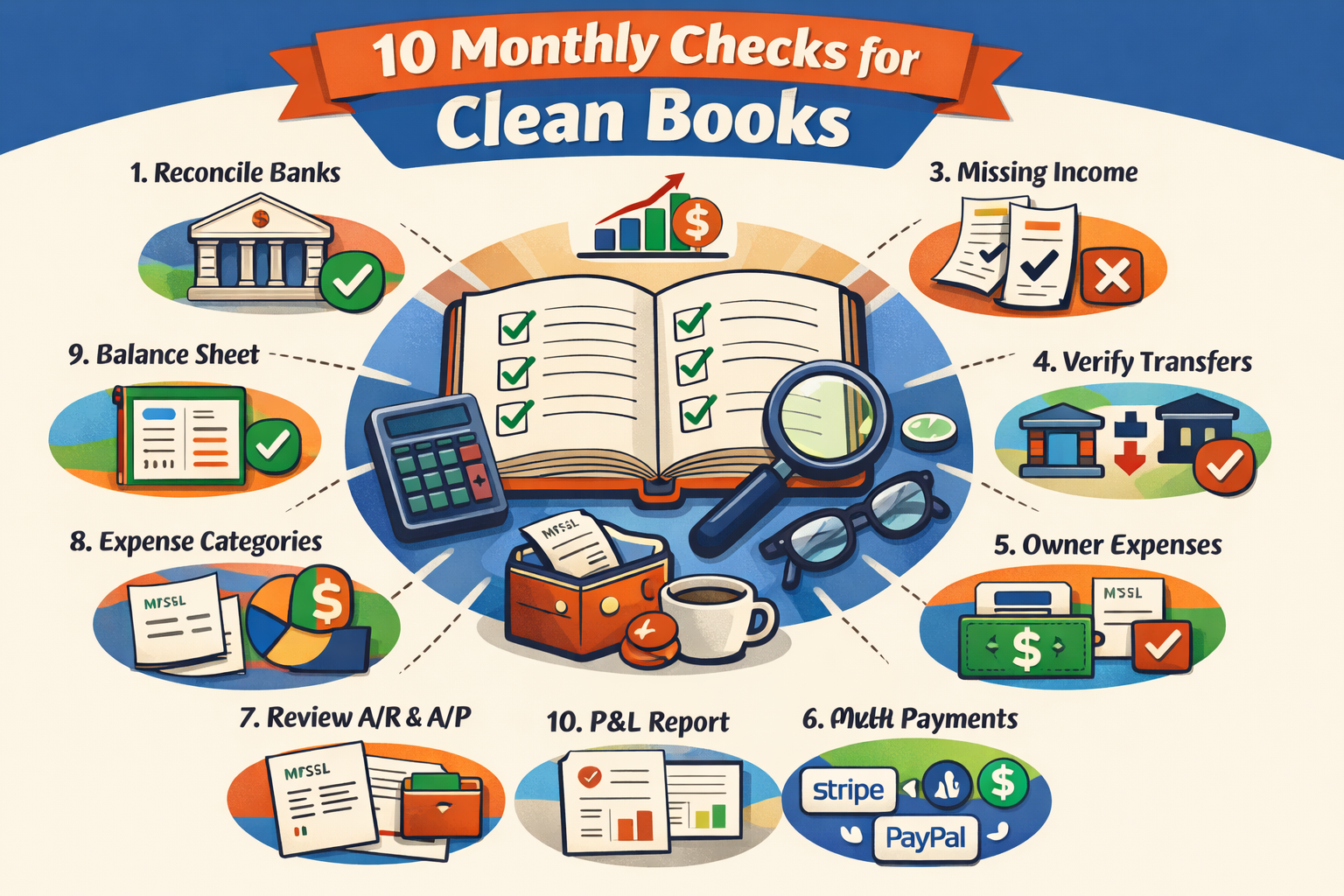

Below are 10 practical monthly checks that professional bookkeepers run to keep books in order. These aren't just technical steps — they catch the issues that cause stress later.

The 10 Monthly Quality Checks

1. Full bank & credit card reconciliation

Every bank account, credit card, and line of credit is matched transaction-by-transaction to the statement. This catches missing deposits (e.g., a client paid but it’s not recorded), uncleared checks, surprise bank fees, and duplicate imports from feeds. Why it matters: mismatched cash balances lead to wrong decisions about how much money is actually available.

2. No duplicate transactions

Search for identical amounts & dates (or very close) in the same account. Duplicates often appear from double-imported feeds, manual entry + auto-import, or re-processing the same Stripe batch. Why it matters: even one $500 duplicate doubles an expense and quietly destroys profit accuracy.

3. All revenue captured (no missing deposits)

Cross-check total monthly deposits (bank + Stripe/PayPal/Square summaries) against recorded sales. Look especially at bundled merchant deposits — they often split into fees + net, and one part can get missed. Why it matters: understated revenue means overstated taxes paid or missed growth signals.

4. Transfers & internal movements correctly handled

Owner transfers between accounts, loan draws, or payments from personal to business are marked as transfers (not income/expense). Why it matters: treating an owner transfer as “misc income” inflates revenue; treating it as expense deflates profit — both distort reports.

5. Owner & personal expenses properly separated

Review any transactions tagged to owner draw, equity, or reimbursements. Confirm nothing personal (groceries, family travel) slipped into business expenses. Why it matters: IRS loves this during audits — mixing personal & business is one of the fastest ways to trigger scrutiny.

6. Prepaids & accruals adjusted

Insurance, rent, or software paid upfront is amortized monthly; utilities or bonuses earned but unpaid are accrued. Why it matters: without this, one month looks artificially good or bad, making trends unreliable.

7. Payroll & tax liabilities match reality

Payroll summary matches QuickBooks liability accounts; quarterly 941/940 estimates align with actual filings. Why it matters: under-recorded payroll taxes create sudden large bills months later.

8. Fixed assets & depreciation current

New equipment added, old assets disposed, monthly depreciation posted. Why it matters: missing depreciation quietly overstates profit and creates tax surprises at year-end.

9. Suspense / uncategorized cleared out

No transactions sit in “Uncategorized Expenses” or suspense accounts by month-end. Why it matters: anything left uncategorized is a red flag — it hides real problems.

10. Key reports reviewed for sanity

Quick look at P&L (profit reasonable?), Balance Sheet (retained earnings makes sense?), Cash Flow (operations positive?). Compare to previous months. Why it matters: numbers can reconcile perfectly but still look wrong at a high level — that’s often the first clue something deeper is off.

Fix this in your books

If you’re not sure where to start, we can help. We’ll review your current bookkeeping setup, identify any gaps or issues, and give you a clear plan to fix it — just straightforward advice.

Red Flags Owners Can Spot Themselves in Reports

- Profit jumps or drops dramatically without clear business reason

- Expenses in one category suddenly much higher than historical average

- Negative cash but positive profit (usually means unreconciled items or accruals missing)

- Large “miscellaneous” or “other” lines on P&L

- Balance sheet shows growing “due to/from owner” without explanation

- Bank balance in QuickBooks differs noticeably from real statement

If you see 2–3 of these, it’s time to ask your bookkeeper for a detailed walkthrough of the last close.

5 Questions to Ask Your Bookkeeper Every Month

- Were all bank and payment platform accounts fully reconciled this month? Any open items?

- Did you find and remove any duplicates or missing transactions?

- Are owner draws/transfers clearly separated from operating expenses?

- Have prepaids, accruals, and depreciation been adjusted?

- Do the P&L and Balance Sheet look reasonable compared to last month and budget?

Good bookkeepers welcome these questions — it shows you care about quality.

Short Example Scenario

A small e-commerce owner notices profit looks great in October, but cash is tight. Bookkeeper runs the 10 checks and finds:

- Two duplicate Stripe imports from a feed glitch → $1,800 extra expense removed

- A $2,500 owner transfer marked as “advertising” → reclassified to equity

- Missing $900 deposit from a late PayPal payout → added to revenue

- Insurance premium not amortized → adjusted $400 expense reduction

Net result: profit decreased by ~$1,100 (more realistic), cash position clarified, and owner avoided overpaying estimated taxes. One monthly review prevented a $3,000+ surprise later.

Ready for Cleaner Books?

If you’re unsure whether your books are truly clean, start with a simple review. Use the site form to request a quick checklist-based assessment—so you know what to fix first.

«What You Get From Monthly Bookkeeping (Deliverables + Quality Standards)».

«Three Common Bookkeeping Mistakes Small Business Owners Make».

«Why Every Business Needs Bookkeeping».

Related services

See how ongoing bookkeeping works.

Fix old months before they create bigger problems.

Compare bookkeeping, QuickBooks, payroll, and reporting support.