In many small businesses, bookkeeping is treated as a compliance task: “as long as it’s ready for tax season, we’re fine.” In reality, accurate books serve a different purpose. They give you a reliable picture of the business, support cash-flow control, and reduce tax and reporting risk. When bookkeeping is done inconsistently or without a clear process, issues build up quietly. Most clients notice it in three ways: reports stop matching reality, decisions are made without dependable numbers, and year-end cleanup takes far more time (and costs more) than it should. Below are three of the most common bookkeeping mistakes we see—and why addressing them early makes a meaningful difference.

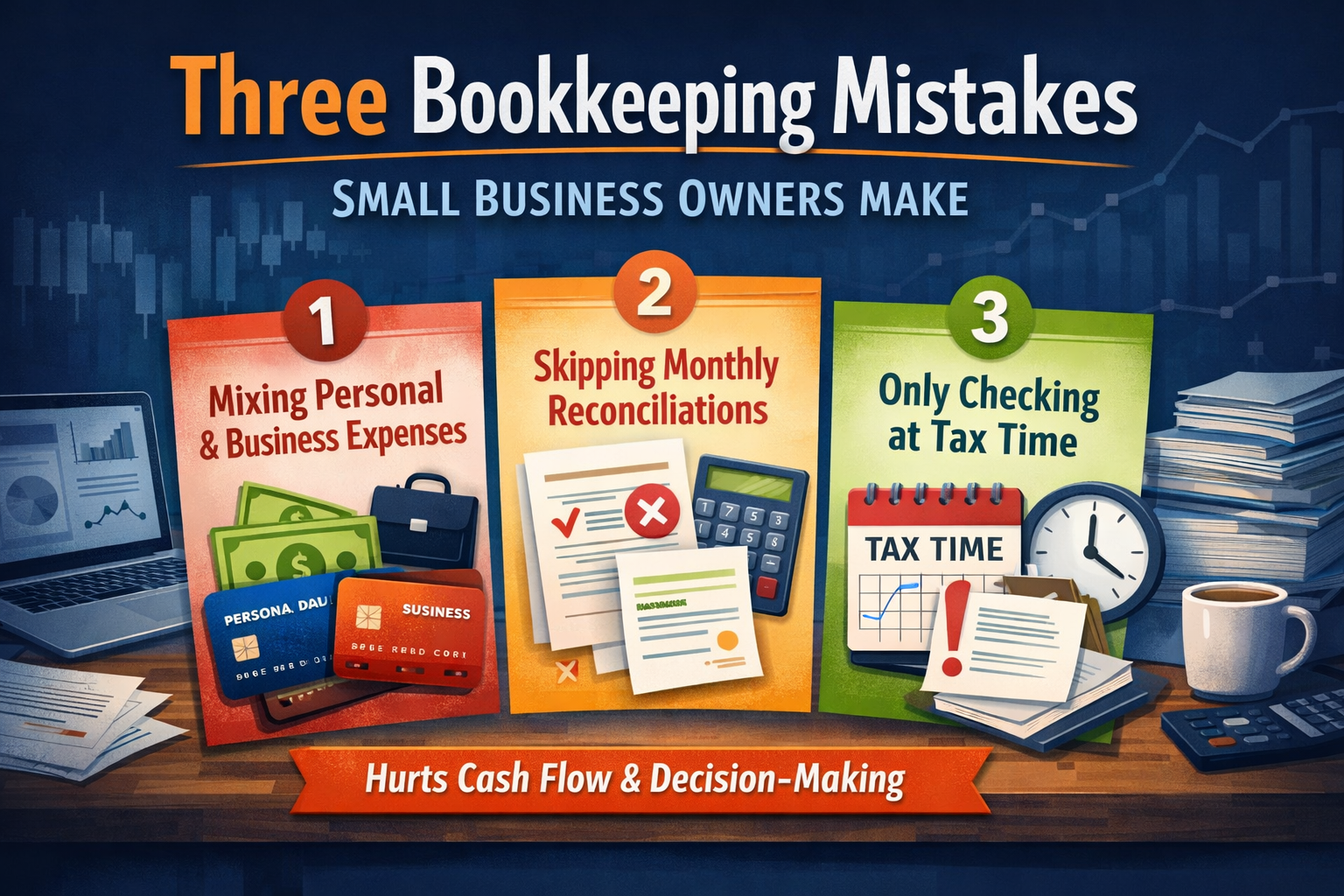

1. Mixing Personal and Business Transactions

This usually starts small: a personal purchase on the business card, a quick transfer between accounts with no memo, or a personal subscription running through the company “just for now.” Over time, those transactions blur the financial picture.

The main issue is that your reports become less useful for management. Expense categories get distorted, margins are harder to evaluate, and it becomes difficult to understand what the business truly costs to operate. It can also create tax friction—because business deductions are harder to support when personal spending is mixed in.

A clean setup is straightforward: keep a separate business bank account and card, and record owner-related activity properly (for example, owner draws/distributions, owner contributions, or reimbursements). When those rules are in place, the books are clearer and tax preparation becomes far more predictable.

2. Skipping Monthly Reconciliations

Even if your bank feed is connected and transactions import automatically, that does not guarantee accurate books. Automation can’t confirm that every item is classified correctly, and it won’t catch every mismatch with your actual bank and credit card statements.

Reconciliation is the process that verifies your bookkeeping matches what actually happened in the bank. When reconciliations aren’t done monthly, common issues appear: missing fees and interest, duplicate transactions, unrecorded refunds, uncategorized items, and balances that don’t tie out.

The result is simple: you end up with reports you can’t rely on—especially if you’re using your P&L to price services, manage expenses, or track profitability. The longer reconciliations are delayed, the more likely you’ll need a full cleanup later.

3. Only Looking at the Numbers During Tax Season

The third issue is the lack of ongoing financial review throughout the year. When business owners only revisit the books at tax time, problems have already accumulated—and fixing them becomes a time-consuming project.

What we typically see at year-end: miscategorized expenses, income and expense gaps, unclear owner transfers, and unresolved credit card activity. At that point, bookkeeping shifts from routine maintenance to damage control.

A better approach is to treat bookkeeping as a monthly cycle: close out each month, reconcile accounts, and do a basic review of categories and reports. When that rhythm is in place, tax season becomes the final step—not the starting point.

Fix this in your books

If you’re not sure where to start, we can help. We’ll review your current bookkeeping setup, identify any gaps or issues, and give you a clear plan to fix it — just straightforward advice.

Bottom Line: Bookkeeping Should Support Better Decisions

Good bookkeeping isn’t about perfection. It’s about having a consistent system that keeps the numbers reliable.

When your books reflect reality, you gain three practical advantages:

1. clearer insight into income and expenses;

2. better cash-flow control and visibility into obligations;

3. lower risk—and fewer costly corrections at year-end.

In most cases, improvement starts with the basics:

separating personal and business activity, reconciling monthly, and reviewing key reports regularly. Those steps deliver the biggest return with the least complexity.

Related services

See how ongoing bookkeeping works.

Fix old months before they create bigger problems.

Compare bookkeeping, QuickBooks, payroll, and reporting support.